Most families think they’re being smart when they pass assets down early.

A parent gifts stock to a child to “help them get ahead.”

A grandparent transfers a rental property to avoid future headaches.

Someone says, “Better to give it now than deal with probate later.”

It feels generous.

It sounds efficient.

And in many cases… it’s a tax disaster in slow motion.

The problem is simple: gifts and inheritances are taxed very differently, and the Tax difference doesn’t show up until years later — usually when the asset is sold and the IRS comes knocking.

This isn’t about loopholes or fancy trusts. It’s about understanding one deceptively boring concept that changes everything: cost basis.

Why This Topic Actually Matters (A Lot)

Generational wealth doesn’t disappear because of bad investments alone. It disappears because of bad timing and misunderstood tax rules.

Families:

- Give assets too early

- Transfer the wrong assets

- Ignore cost basis entirely

- Focus on estate tax (which most people don’t even owe)

- Miss the massive advantage inheritances have over gifts

The irony? Many people gift assets to save taxes and end up increasing them instead.

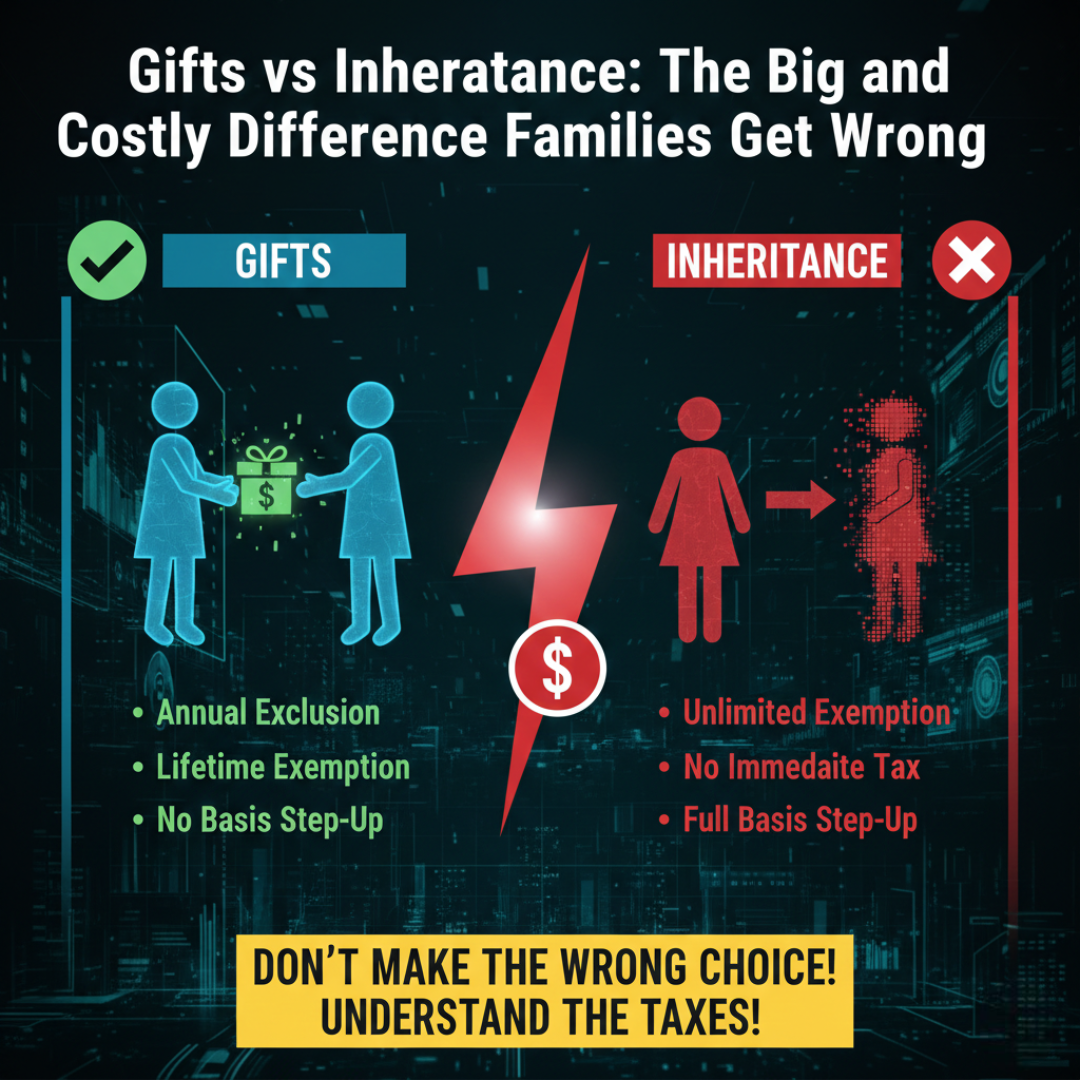

The Core Difference (In Plain English)

When someone receives an asset, the IRS asks one question later when it’s sold:

“What was it worth when you got it?”

The answer depends entirely on whether it was a gift or an inheritance.

Inheritance = Step-Up in Basis

Gift = Carryover Basis

Those two phrases decide how much tax gets paid — not love, intention, or family tradition.

Inheritance: The Step-Up Basis Advantage

When you inherit an asset, you usually receive a step-up in cost basis.

That means the IRS pretends the asset was “bought” at its fair market value on the date of death.

Not what your parents paid.

Not what it was worth decades ago.

What it was worth then.

Simple Example

Your parents bought stock for $20,000 in the 1990s.

It’s worth $200,000 when they pass away.

You inherit it.

Your new cost basis: $200,000.

If you sell it shortly after for $205,000, you’re taxed only on $5,000.

That’s not a loophole. That’s how the system is designed.

Gifts: The Carryover Basis Trap

Gifts look similar on the surface, but tax-wise they are a different species entirely.

When someone gifts you an asset, you inherit their original cost basis, not the current value.

Same stock. Same family. Very different outcome.

Same Example, Gift Version

Parents bought stock for $20,000.

It’s worth $200,000 today.

They gift it to you.

Your cost basis: $20,000.

You sell it for $205,000.

Your taxable gain: $185,000.

Same asset. Same sale price.

180,000 difference in taxable income.

That’s not a rounding error. That’s tuition-level money.

Why Families Get The Tax Difference Backwards

There are a few common reasons this mistake keeps happening.

1. Estate Tax Fear

People still believe estate tax applies to “normal” families.

In reality, federal estate tax only hits estates above very high thresholds. Most families never come close.

But fear drives behavior — and fear causes early gifting.

2. “Avoid Probate” Panic

Probate is inconvenient, not catastrophic.

Families often gift assets early to avoid paperwork later, without realizing they’re trading mild legal friction for massive tax exposure.

3. Emotional Logic Beats Financial Logic

Giving while alive feels more meaningful.

Seeing kids enjoy the asset feels rewarding.

That emotional win sometimes blinds people to long-term consequences.

Real-World Scenario: The Helpful Parent Mistake

A parent gifts their adult child a rental property worth $500,000.

They bought it decades ago for $120,000.

Years later, the child sells it.

They don’t just pay capital gains tax on appreciation.

They also face depreciation recapture, stacked on top.

The parent thought they were helping.

The child inherits a tax bomb instead.

Had the property been inherited instead of gifted, most of that tax exposure could’ve vanished instantly.

When Gifting Does Make Sense

This isn’t a “never gift anything” rule. Context matters.

Gifting can make sense when:

- The asset has low appreciation

- The recipient is in a very low tax bracket

- The asset is unlikely to be sold

- The goal is cash flow, not liquidation

- Estate size truly exceeds tax thresholds

The mistake is gifting highly appreciated assets without understanding the downstream tax cost.

The Overlooked Middle Ground: What to Gift Instead

Here’s where smart planning quietly wins.

Instead of gifting:

- Appreciated stocks

- Real estate

- Long-held investments

Families often do better gifting:

- Cash

- Low-basis assets last

- Assets inside Roth accounts

- Annual exclusion gifts for expenses

Let the high-growth, high-appreciation assets get the step-up later.

How Capital Gains Multiply the Mistake

The pain doesn’t stop at capital gains tax.

Large gains can also:

- Push heirs into higher tax brackets

- Trigger Medicare IRMAA surcharges later

- Increase taxation of Social Security

- Eliminate credits and deductions

One gifting decision can echo for decades.

Documentation: The Silent Dealbreaker

Even when inheritance rules apply, lack of documentation can undo everything.

Without:

- Date-of-death appraisals

- Clear ownership records

- Proper estate documentation

The IRS may challenge basis assumptions.

Families that plan well but document poorly still lose.

The Generational Planning Mindset Shift

The biggest shift families need to make is this:

It’s not about who gets the asset.

It’s about when they get it.

Timing can matter more than generosity.

Inheritance isn’t cold or selfish.

It’s often the most tax-efficient form of giving.

Common Myths That Need to Die Quietly

“Gifting avoids taxes.”

Sometimes it increases them.

“Estate tax is the real danger.”

For most families, it isn’t.

“The IRS will never notice.”

They always notice asset sales.

How to Make a Smarter Family Plan

Good generational planning answers three questions:

- Which assets should be inherited?

- Which assets can safely be gifted?

- When does timing matter more than intent?

This isn’t about hoarding wealth.

It’s about not accidentally burning it.

Final Thoughts: Generosity Without Strategy Is Expensive

Families don’t lose money because they’re careless.

They lose it because nobody explains these rules in human language.

Gifting feels right.

Inheritance feels distant.

But from a tax perspective, inheritances often protect families far better than gifts ever could.

Understanding the difference doesn’t make you less generous.

It makes your generosity last longer.

And in generational planning, lasting is the whole point.

Before making any decision about gifting or inheriting assets, it helps to see the tax impact in real numbers. You can use our Capital Gains Tax Calculator on CapitalTaxGain.com to estimate potential taxes based on purchase price, sale value, and timing — so your family can plan with clarity instead of surprises.

Leave a Reply