Selling your business is often framed as the finish line. Cash in, walk away, start the next chapter. But tax-wise, it’s more like opening a trapdoor you didn’t know was there.

Business owners routinely lose six or seven figures to taxes simply because they didn’t understand how the sale would be taxed before signing the deal.

This isn’t about loopholes or tricks. It’s about understanding how the system actually works — and using the options it already gives you, to understand how to avoid the tax shock.

Why Business Sales Trigger Massive Tax Bills

Here’s the core problem: selling your business isn’t taxed as one simple transaction.

It’s usually treated as a bundle of sales happening all at once.

That bundle might include:

- Equipment

- Inventory

- Customer lists

- Contracts

- Brand value

- Goodwill

Each piece can be taxed differently.

Some are taxed as capital gains.

Some are taxed as ordinary income.

Some trigger depreciation recapture (which feels especially cruel).

Most owners don’t realize this until the tax bill arrives.

The First Big Mistake: Assuming “Sale Price = Capital Gains”

This is where expectations go to die.

If you sell your business for $2 million, you do not automatically pay capital gains tax on $2 million.

Your taxable gain depends on:

- Your cost basis (what you invested over time)

- How the sale price is allocated

- The structure of the deal

- Whether payments come all at once or over time

Two owners can sell identical businesses for the same price and walk away with wildly different after-tax outcomes.

Asset Sale vs Stock Sale: The Fork in the Road

This decision alone can change your tax bill by hundreds of thousands of dollars.

Asset Sale

Most buyers prefer asset sales. Why?

- They get a fresh depreciation schedule

- They avoid inheriting liabilities

But for sellers, asset sales often mean:

- More income taxed at ordinary rates

- Depreciation recapture

- Higher overall tax burden

Stock (or Equity) Sale

Sellers usually prefer stock sales because:

- Most of the gain is taxed as long-term capital gains

- Fewer layers of taxation

- Cleaner exit

The problem? Buyers often resist.

This creates a negotiation — not just on price, but on tax consequences.

Many sellers focus entirely on the headline number and ignore the after-tax reality. That’s how you “win” the deal and still feel robbed later.

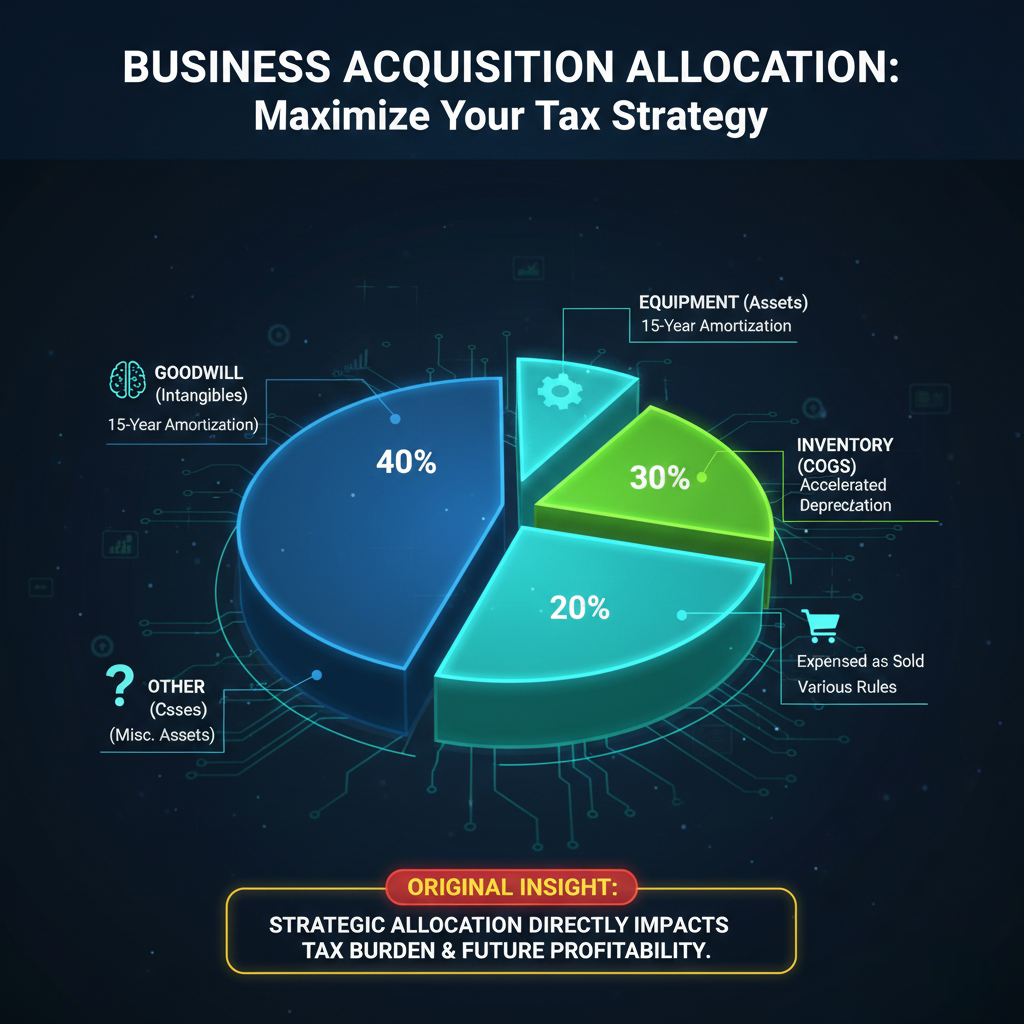

Asset Allocation: The Quiet Tax Multiplier

Even if the deal type is set, how the sale price is allocated matters more than people realize.

The IRS requires both parties to agree on how the purchase price is split across assets. That allocation determines how each portion is taxed.

For example:

- Inventory → ordinary income

- Equipment → depreciation recapture

- Goodwill → capital gains

Buyers want more allocated to assets they can depreciate quickly.

Sellers want more allocated to goodwill.

This is not a formality. It’s one of the most important tax decisions in the entire transaction.

And once it’s signed? It’s very hard to undo.

The Emotional Trap: “I Just Want Out”

This is where people make expensive mistakes.

By the time a sale is on the table, many owners are exhausted.

Burned out.

Ready to move on.

So they rush.

They stop asking questions.

They stop modeling outcomes.

They stop pushing back.

That emotional urgency can cost more than bad investing ever could.

Installment Sales: Turning One Big Tax Hit Into Manageable Ones

Here’s one of the most underused — and misunderstood — tools available to sellers.

An installment sale means you don’t receive the full purchase price upfront. Instead, payments are spread over time.

Tax-wise, this means:

- You recognize gain as payments are received

- Your income is spread across multiple years

- You may stay in lower tax brackets

- You reduce the shock effect on benefits and surtaxes

This doesn’t eliminate tax.

It reshapes it.

Installment sales can be especially powerful if:

- You’re nearing retirement

- You expect income to drop

- You want predictable cash flow

- You’re trying to avoid Medicare IRMAA surcharges

Not every deal allows for this, but many do — especially private sales.

Reinvestment Strategies: Deferral vs Illusion

Let’s clear up a common myth right away.

Reinvesting the money does not cancel capital gains tax.

Selling is the taxable event. What you do with the proceeds afterward doesn’t change that.

That said, certain reinvestment strategies can defer or reduce taxes in specific cases.

Depending on the situation, options may include:

- Structured installment notes

- Opportunity Zone investments

- Retirement-focused transitions

- Charitable planning strategies

Each has trade-offs. None are magic. Some are overhyped.

The key is understanding whether you’re deferring tax, reducing tax, or just moving it around.

The “All-in-One-Year” Problem

Here’s what often causes the worst outcomes:

- Large business sale

- Paid in full

- Same year as other income

- No offsetting losses

- No planning window

That one year becomes a financial spike:

- Highest tax bracket

- Net Investment Income Tax

- State taxes

- Benefit phaseouts

- Medicare premium increases (two years later)

The money arrives quickly.

The costs linger.

A Simple Scenario (That Happens Constantly)

Let’s say:

- You sell your business for $3 million

- Your cost basis is low

- Most of the deal closes in one year

You expect capital gains tax.

You don’t expect:

- A higher effective tax rate than anticipated

- Medicare premiums jumping later

- Social Security taxation increasing

- State taxes stacking on top

- Cash flow tightening post-sale

The surprise isn’t the tax itself.

It’s how many systems respond to that income.

What Smart Sellers Do Differently

The difference isn’t intelligence.

It’s timing and structure.

Smart sellers:

- Run projections before signing

- Model multiple sale structures

- Negotiate allocation intentionally

- Spread income where possible

- Plan benefits alongside taxes

- Accept slightly lower prices for better after-tax outcomes

A $100,000 lower sale price can still leave you richer if it saves $300,000 in tax.

This Is Not a DIY Moment

Selling a business is one of the rare times when:

- CPA advice pays for itself

- Legal structure matters

- Small details create massive consequences

This isn’t about hiring someone to “do your taxes.”

It’s about involving them before the deal closes.

Once the sale is finalized, options collapse fast.

The Mental Reframe That Changes Everything

Don’t ask:

“How much can I sell this for?”

Ask:

“How much do I keep after everything reacts to this sale?”

That single shift changes:

- Negotiation priorities

- Deal structure

- Timing

- Peace of mind

Final Thoughts: The Sale Is Not the End — It’s a Transition

Selling a business is not a finish line.

It’s a handoff.

From one form of wealth…

to another.

When done without planning, taxes feel like punishment.

When done intentionally, they become just another variable you control.

Capital gains tax shock isn’t inevitable.

It’s predictable.

And predictability is power.

If you’re selling a business — or even thinking about it — the best time to plan was yesterday. The second-best time is before you sign anything that locks your future into a single, very expensive year.

Before finalizing any business sale, it’s worth seeing the full after-tax picture — not just the purchase price. Our Capital Gains Tax Calculator on CapitalTaxGain.com helps you estimate potential gains and taxes based on your sale details, so you can understand the impact before a deal turns into an expensive surprise.

When planning the sale of your business, it’s important to understand how different assets are taxed and how deal structure affects your capital gains. The IRS provides detailed guidance on how to report and calculate gains from business asset sales in Publication 544, while the Small Business Administration offers practical advice on tax strategies when selling a business. For owners of qualified small business stock, resources like Investopedia’s Section 1202 guide explain how you may exclude a significant portion of gains under certain conditions. Reviewing these resources can help you plan your sale more effectively and avoid unexpected tax shocks.

Leave a Reply