When you inherit assets—whether it’s a family home, stocks, or a piece of artwork—you might assume you’re simply receiving a gift from your loved ones. What many people don’t realize is that the timing and valuation of those assets can dramatically affect your tax situation, sometimes saving you thousands—or costing you more than you expected.

This is where the step-up in basis becomes crucial. Understanding it isn’t just tax trivia; it’s a way to protect your inheritance, make smarter decisions about selling, and avoid unnecessary capital gains taxes. Let’s break it down in plain English, with real examples, storytelling, and practical tips.

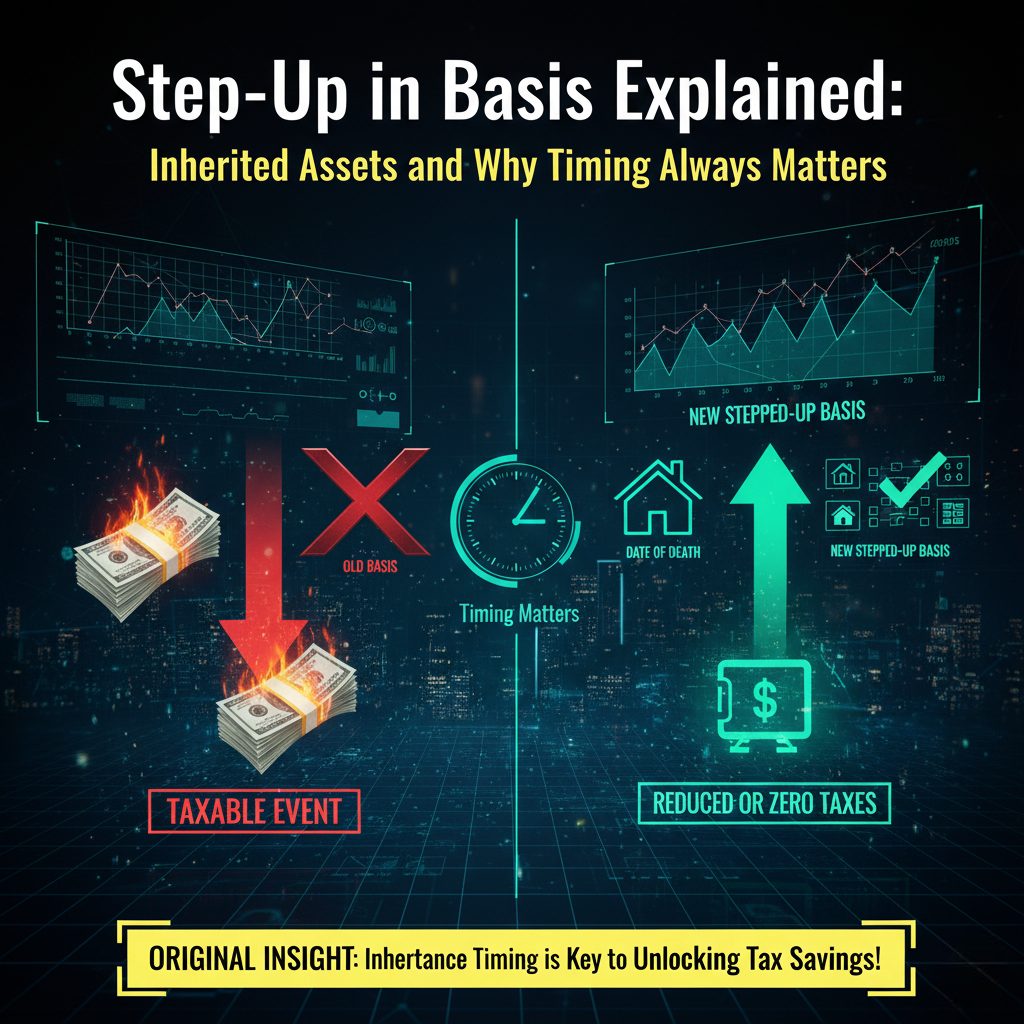

What Step-Up in Basis Actually Means

Step-up in basis is a tax concept designed to ease the burden on heirs. Simply put:

When you inherit an asset, your cost basis is “stepped up” to its fair market value at the time of the original owner’s death.

That means you’re not taxed on the appreciation that occurred during the decedent’s lifetime. You only owe capital gains tax on any increase in value from the date of inheritance to the date you sell.

Example:

- Grandma bought a home for $50,000 in 1980.

- When she passed away in 2020, it was worth $400,000.

- You inherit it. Your cost basis is $400,000, not $50,000.

- If you sell for $420,000, you pay tax only on the $20,000 gain, not the $370,000 appreciation over 40 years.

Without a step-up, heirs could face enormous capital gains bills, paying tax on decades of unrealized appreciation.

Why Timing Matters: The Devil’s in the Dates

Step-up in basis is not automatic in every scenario. Timing and documentation are key.

1. Market Fluctuations Affect Your Step-Up

The step-up is based on the fair market value (FMV) on the date of death. If markets are volatile, the same asset can step up to a higher or lower value depending on when the owner passes.

Example:

- Stock portfolio valued at $100,000 when Grandpa passes.

- A market rally the next month would have increased it to $120,000.

- But for step-up purposes, your basis is $100,000, not the higher amount you might have wished for.

This is why timing can feel cruel—assets you inherit might seem “cheap” on paper if markets dipped.

2. Gifts vs Inheritance: Step-Up Doesn’t Always Apply

Many families assume that gifts are treated the same as inherited assets. They’re not.

- Gifted assets: Your cost basis is generally the donor’s original cost basis, not the current FMV. If a parent gives you stock purchased decades ago, you could owe tax on the entire appreciation when you sell.

- Inherited assets: Step-up applies, so you start fresh at the FMV on the date of inheritance.

Lesson: If your goal is to reduce capital gains taxes for heirs, waiting until inheritance rather than gifting can be far more tax-efficient.

3. Documentation and Appraisal Are Critical

Step-up only works if the IRS can verify the FMV at the time of death. That means:

- Appraisals for real estate or unique assets

- Brokerage statements for stocks

- Estate records for businesses or collectibles

Without proper documentation, the IRS might challenge your reported basis, leaving you liable for taxes you expected to avoid.

Step-Up in Basis and Different Types of Assets

Real Estate

Real estate is the most common asset where step-up matters.

- Primary residences often combine the step-up with the $250K/$500K exclusion for capital gains if you lived there, making this a powerful tool.

- Rental properties also step up, but without the personal-use exclusion. Planning your sale and calculating depreciation recapture are essential.

Stocks and Bonds

Publicly traded assets are easier to value, but step-up still matters:

- Stocks with decades of appreciation: step-up can reduce a multi-year gain to nearly zero.

- Bonds or mutual funds: inherited bonds often adjust basis to FMV at death, reducing taxable gain when sold.

Collectibles, Art, and Businesses

These assets are trickier:

- The IRS may require professional appraisals for high-value artwork or collectibles.

- Family-owned businesses have complex valuation rules, and step-up can significantly reduce tax bills, but timing and documentation are everything.

Real-Life Example: When Step-Up Makes a Huge Difference

Consider this scenario:

- Uncle Sam bought a small business for $20,000 in 1990.

- At his death in 2025, the business is worth $500,000.

- You inherit it.

- Your cost basis steps up to $500,000.

If you sell immediately for $500,000: $0 capital gains tax.

If Uncle had gifted it instead: Your basis would be $20,000, and your capital gains could exceed $480,000, taxed at the top rate—potentially hundreds of thousands in taxes avoided with proper step-up planning.

Step-Up Pitfalls to Avoid

- Assuming it applies automatically

Always verify the type of asset and ownership structure. - Failing to document properly

Appraisals, statements, and estate records are your defense against IRS audits. - Ignoring state taxes

Some states don’t follow federal step-up rules, so you may still owe local capital gains taxes. - Joint ownership complications

Only the deceased’s portion may step up. Married couples with joint assets require careful attention.

Planning Ahead: How to Maximize the Step-Up

1. Don’t Sell Immediately

If markets are down at the time of inheritance, consider waiting for an appropriate opportunity to sell. Step-up protects you from gains before the date of death, but your FMV might be temporarily depressed.

2. Consider Timing Gifts Carefully

Transferring assets as gifts may trigger capital gains for the recipient. In many cases, inheritance is far more efficient.

3. Coordinate with a CPA or Estate Planner

Professional guidance ensures you:

- Document the FMV properly

- Understand potential tax traps

- Align inheritance planning with your financial goals

Why Step-Up in Basis Changes Retirement and Estate Planning

Step-up isn’t just a tax rule—it’s a financial strategy. It influences decisions such as:

- When to sell inherited property

- How to structure gifting for children or grandchildren

- How to manage family-owned businesses for minimal tax impact

- Timing sales in volatile markets

By planning around step-up, heirs can preserve wealth and reduce tax bills without breaking any laws.

Final Thoughts

Step-up in basis is one of the most powerful yet underused tools in estate planning. It transforms the way you think about inherited assets—not just as sentimental items, but as financial instruments that can either generate wealth or create unexpected tax bills.

Timing matters. Documentation matters. Strategy matters.

By understanding step-up in basis, planning asset sales carefully, and consulting professionals when needed, you can protect your inheritance, honor your family’s legacy, and avoid unnecessary taxes.

Inheritance isn’t just about receiving assets. It’s about making them work for you, legally and efficiently.

Before selling any inherited assets, it’s wise to see the numbers clearly. Our Capital Gains Tax Calculator at CapitalTaxGain.com lets you plug in your inherited asset values, sale price, and holding period to estimate taxes before you sell—helping you plan smarter and avoid surprises.

On the official IRS site, Publication 551 (“Basis of Assets”) explains how the basis of property you inherit is determined. It confirms that the fair market value at the date of the decedent’s death usually becomes your cost basis, which can eliminate capital gains tax on appreciation that happened before you inherited the asset. The publication also covers alternate valuation dates and how basis is reported and used when filing taxes.

Leave a Reply