Capital gains tax used to be boring. Buy something, sell it later, pay a percentage, move on with life.

With Capital Gains Tax in 2026, that illusion is officially dead.

Across markets — especially in India, but increasingly worldwide — equity, bonds, and gold are no longer playing by the same tax rules. The holding period that counts as “long term” isn’t consistent. The rates aren’t aligned. Indexation helps some assets and is completely useless for others. And certain instruments that used to feel tax-friendly have quietly become tax landmines.

That’s why investors keep getting surprised. Not because they’re careless — but because the system has fractured.

This piece is about clarity. No jargon soup. No tax-bro flexing. Just a clean breakdown of how capital gains work in 2026 depending on what you own, why the differences exist, and what they mean for real humans making real decisions.

First, a quick reset: what “capital gains” actually means

A capital gain is the profit you make when you sell an asset for more than you paid for it.

Simple enough.

Where things get spicy is how governments decide to tax that profit. They usually care about three things:

- What kind of asset it is

- How long you held it

- Whether inflation adjustments apply

Change any one of those, and the tax bill changes — sometimes dramatically.

In 2026, those rules diverge sharply between equity, bonds, and gold.

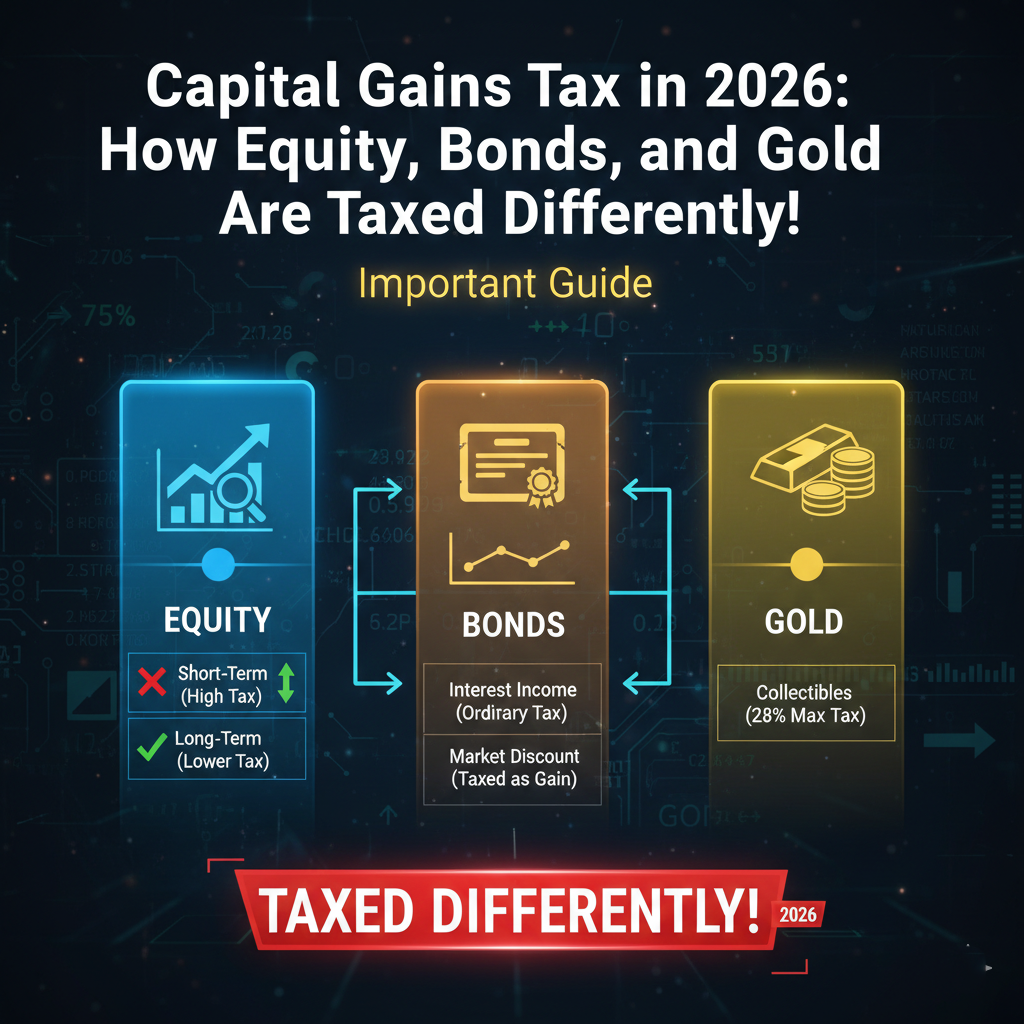

Equity (Stocks, Equity Mutual Funds): Still favored, but with fine print

Let’s start with equity, because it’s still the golden child — just a little less golden than people assume.

How equity gains are taxed in 2026 (India-focused, globally relevant logic)

For listed equities and equity-oriented mutual funds:

- Short-term capital gains (STCG)

If you sell within 12 months, gains are taxed at a flat rate (commonly 15% in India, similar preferential treatment elsewhere). - Long-term capital gains (LTCG)

After 12 months, gains above the exemption threshold are taxed at a lower rate (10% in India), without indexation.

This structure exists because governments want to encourage participation in capital markets. Equity fuels businesses, employment, and economic growth. Tax incentives are the carrot.

The quiet catch people miss

No indexation.

That means inflation doesn’t reduce your taxable profit. If inflation eats half your “real” return, the tax system shrugs and taxes the full nominal gain anyway.

In a low-inflation world, that’s fine. In a high-inflation decade, it matters a lot.

So equity is still tax-efficient — but only if your returns comfortably beat inflation.

Bonds and Debt Funds: The tax efficiency illusion is gone

Debt used to be the calm, sensible sibling. Predictable returns. Lower volatility. Often indexation benefits that softened the tax blow.

That era is mostly over.

What changed — and why it matters in 2026

In recent rule changes, many debt mutual funds lost long-term capital gains benefits entirely.

For a large category of bonds and debt funds:

- Gains are now taxed at your slab rate

- Holding period doesn’t rescue you

- Indexation doesn’t apply

In practical terms, this means debt income is being treated more like salary, not investment growth.

Why governments did this

Debt instruments were being used as tax shelters rather than income products. Indexation made modest returns look tax-free over time. Governments noticed. Governments adjusted the rules.

The result:

Two investors earning the same return — one through equity, one through debt — can now face radically different tax outcomes.

What this means for investors

Debt still has a role:

- Stability

- Cash flow

- Risk management

But from a tax perspective, it is no longer automatically efficient. You now have to evaluate debt returns after tax, not before.

In 2026, ignoring this difference is one of the most common portfolio mistakes.

Gold: The most misunderstood tax story of all

Gold feels simple. Buy gold. Hold it. Hedge inflation. Sell later.

Tax authorities, however, see multiple versions of “gold,” and they tax each one differently.

Physical gold & gold ETFs

Traditionally:

- Short-term gains taxed at slab rates

- Long-term gains taxed with indexation benefits

This made gold attractive as a long-term inflation hedge, because indexation often wiped out a big chunk of the taxable gain.

Sovereign Gold Bonds (SGBs): where 2026 gets interesting

SGBs were long marketed as tax-friendly. And they still are — but only if you play by very specific rules.

If you hold SGBs until maturity, capital gains are typically tax-exempt.

But here’s the 2026 reality check:

If you sell SGBs on the secondary market, recent rules mean:

- Gains can be taxed like other capital assets

- Exemptions may not apply

- The tax treatment can differ from what investors originally assumed

This has caught many people off guard. They bought SGBs thinking “tax-free,” sold early for liquidity, and discovered the exemption didn’t follow them out the door.

The lesson gold keeps teaching

Gold taxation depends heavily on how you own it and how you exit.

Physical gold, ETFs, SGBs — same underlying metal, wildly different tax math.

Why asset classes are diverging instead of converging

This isn’t accidental. It’s policy.

Governments use capital gains rules to shape behavior:

- Encourage equity investment → lower rates

- Discourage tax arbitrage → remove indexation where abused

- Control speculative behavior → short-term penalties

- Reward patience → selective long-term benefits

In 2026, tax codes are becoming behavioral tools, not just revenue tools.

That’s why the same ₹1,000,000 gain can be taxed three different ways depending on whether it came from stocks, bonds, or gold.

A simple comparison (no spreadsheets required)

Think of it this way:

Equity rewards risk and growth

Debt taxes income and predictability

Gold taxes structure and timing

None of them are “good” or “bad” universally. They’re context-dependent.

The mistake is assuming the tax logic of one asset applies to another.

The real danger: mixing assets without forecasting taxes

Most portfolios are mixed. Equity + debt + some gold. Sensible.

But taxes aren’t calculated on the portfolio — they’re calculated asset by asset.

This is how investors end up shocked:

- Equity gains push income over thresholds

- Debt gains taxed at high slab rates

- Gold sales triggering unexpected capital gains

- Total tax bill far higher than expected

The problem isn’t diversification. It’s lack of forecasting.

Why Capital Gains Tax in 2026 demands better planning than ever

Markets are volatile. Inflation isn’t dead. Tax rules are evolving faster than investor habits.

In this environment, guessing your tax outcome is expensive.

Smart investors in 2026 are doing one simple thing differently:

They estimate capital gains before they sell — not after.

That single habit prevents:

- Panic selling

- Threshold breaches

- Overpaying tax due to bad timing

- Regret trades that looked good pre-tax and awful post-tax

One last grounding thought

Capital gains tax isn’t a punishment. It’s a signal.

It tells you what the system wants you to do:

Hold here. Trade there. Take risk in this lane, not that one.

In 2026, equity, bonds, and gold are sending very different signals. Treating them the same is how people lose money quietly.

Understanding the differences doesn’t require a CPA — just clear thinking, decent assumptions, and a willingness to run the numbers before emotions take the wheel.

And in a world where rules keep changing, clarity is the real edge.

Asset classes are taxed differently in 2026, and small timing decisions can change your tax bill by thousands. Our Capital Gains Tax Calculator lets you estimate what you’ll actually owe on equity, bonds, or gold before you sell — no spreadsheets, no guesswork. It’s built to surface surprises early, so you can plan smarter instead of reacting later.

Leave a Reply